New Jersey Governor Phil Murphy (D) signs law to take in effect within 3 months that will reduce Surprise Out-Of-Network Medical Bills.This is well needed and in-step with NYS law passed 3 years ago – No More Surprises – NY Surprise Medical Bill Law.

The reform is designed to protect patients, businesses, and others who pay for medical care from the high-cost bills associated with emergency or unintentional care from doctors or other providers who are not part of their insurance network. The law requires greater disclosure from both insurance companies and providers — so patients are clear on what their plan covers — ensures patients aren’t responsible for excess costs, and establishes an arbitration process to resolve payment disputes between providers and insurers, a mechanism intended to better control costs.

The Problem. This has been a pattern in recent years and posted in Out of Control Out of Network Charges (March 2012). According to an investigation report commissioned by Governor Cuomo recognizing the unexpected out-of-network claim problem. Officials say that this is now “an overwhelming amount of consumer complaints.” Some examples cited in the report An Unwelcome Surprise – “a neurosurgeon charged $159,000 for an emergency procedure for which Medicare would have paid only $8,493.” Another example: ” a consumer went to an in-network hospital for gallbladder surgery with a participating surgeon. The consumer was not informed that a non-participating anesthesiologist would be used, and was stuck with a $1,800 bill. Providers are not currently required to disclose before they provide services whether they are in-network.” The average out-of-network radiology bill was 33 times what Medicare pays, officials say.

The blog post goes on to say “Today, 90% of SMB members have in network only benefits but the few remaining consumers are paying for eroding out of network benefits with little transparencies and necessary protection from new out of network billing practices. The NY Dept of Financial services is calling for providers in non-emergency situations to disclose whether or not all services are in-network, what out-of-network charges will be and how much insurers will cover.”

The Solution: The The out-of-network Consumer Protection, Transparency, Cost Containment and Accountability Act requires greater disclosure from both insurance companies and providers — so patients are clear on what their plan covers — ensures patients aren’t responsible for excess costs, and establishes an arbitration process to resolve payment disputes between providers and insurers, a mechanism intended to better control costs. The law sets a timeline and other parameters for negotiations between the payer and the provider and, if they can’t resolve the issue, requires the state to hire an independent expert to decide between the final offers presented by both sides. While earlier drafts of the bill included a range of factors for the arbitrator to consider in making this decision — including the doctor’s experience, the patient’s condition, and certain payment benchmarks — these details were eliminated entirely in the final version.

NJ becomes the 7th State to enact such consumer protection. The other states include California, Connecticut, Florida, Illinois, Maryland and New York.

Learn how a Private Exchange and our PEO Partnership can help your group please contact us – info@medicalsolutionscorp.com or (855)667-4621.

Empire Blue Cross Blue Shield recently announced their re-entry back into the New York small group market for 2017. A legendary broad networked PPO is welcome news especially in the NY small group market of 1-100 employees. Recently, the broad national networks have diminished to only 2 national health insurers, Aetna and Oxford. As a result of Empire Blue Cross participation in the BlueCard PPO program members enjoy unparalleled national access network to 96% of hospitals and 93% of doctors across the country. This national program will be on 18 of 28 plans below.

PPO/EPO Network – traditional non-gatekeeper large network of approximately 85,384 physicians, 160 facilities and the BlueCard PPO

Blue Priority Network – hybrid of broad PPO/EPO 160 facilities and similar Pathway’s 65,796 physicians network.

Pathway Network – HMO value based narrower gatekeeper referral network of 109 facilities and 60,535 physicians. Limited to 28 NYS Counties.

Additional Features:

Telemedicine will be available on all products

Vision – Limited adult vision will be available on all products at no additional cost.

Pharmacy – All plans use their large BCBS formulary Except the HMOs, and the Silver and Bronze Blue Priority Plans. They will be utilizing what they call the Select Formulary.

Clinical Programs – health coaching/advocacy, disease management, behavioral health, maternity and Gaps in Care

Online Resources – wellness coaching, discounts, health assessments and The Weight Center.

Healthy Support – Wellness program offers easy ways to earn up to $900 per member, per year. Gym Reimbursement $400 single/$600 couple, $100 Wellness + Flu Shot, Online Wellness toolkit, up to $150 and $50 Tobacco-free certification online.

Ask us about Empire’s flexible low participation voluntary group dental, vision, disability and life insurance plans. Stay proactive and contact us today for a customized consult on how your organization can prepare ahead for ACA, Benefits, Payroll and HR @ (855) 667-4621 or info@medicalsolutionscorp.com.

Contact Us Now Learn how our Agency is helping buinsesses thrive in today’s economy. Please contact us at info@medicalsolutionscorp.com or (855)667-4621.

First, Register for a NY GOV ID by clicking as noted below

2. Once you have created your Login credentials, you then have to Login to the site using your new credentials

Once in for the first time, your first screen looks like this:

3. On the next page, under Account and Identity Information, at the bottom of the screen it asks for Broker/Navigator information. Choose ‘YES’ (no cost or higher rates to use a broker, so take advantage of our knowledge for free!) and click on Find a Broker/Navigator/Application Counselor

Broker/Navigator Information

Do you need a Broker/Navigator/Application Counselor ?

Yes No

Selected Broker/Navigator/Application Counselor:

Find a Broker/Navigator/Application Counselor

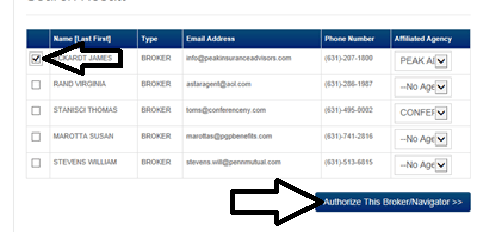

When prompted on the search page, type in Alex Miller where shown in the screenshot below.

In addition, you can alternatively put in zip code 10583 and Alex Miller will show.

You then put a ‘check’ mark next to Alex Miler, then hit ‘Authorize this Broker’ at the bottom left of the search list:

Once you have authorized us as your broker, we get notified on our broker portal. You are not done yet.

NY State of Health Individual Health Insurance

You will need to continue with your application, namely going thru the following questions asked by the NYSOH to identity proof you and make sure you are who you say you are. You can also check to see if you are eligible for any assistance or subsidy during this process. It is only when you get to the last step, ‘FIND A PLAN’, that we can help you.

Account Information

Contact Information

Build Household

Household Members

Relationships

Residential Address

Household Summary

Public MEC

Income Information

Tax Filing Status

Income Details

Income Summary

Other Information

Application Summary

Find a Plan

At this point, you should contact us to let us know you are ready for us to advise you on your medical choices. You might consider having a list of doctors or hospitals you want to check on to see which carriers include these providers in their networks.

With 20+ years’ experience with health insurance you will have all of that knowledge working for you! Wishing you success on securing a good health plan and look forward to helping you in the process.

Stay proactive and contact us today for a custmozied consult on how your organization can prepare ahead for ACA, Benefits, Payroll and HR @ (855) 667-4621 or info@medicalsolutionscorp.com.

ALBANY, NY (October 11, 2018) — NY State of Health, the state’s official health plan Marketplace today announced Qualified Health Plan, Essential Plan, and other options that will be available to consumers in 2019. The 2019 Open Enrollment Period begins November 1, 2018 and will continue through January 31, 2019. Over 95 percent of Marketplace enrollees will see no cost increase in 2019, including those who are enrolled in Medicaid and the Essential Plan and those who are eligible to enroll in a Qualified Health Plan with financial assistance. And New York’s enrollment window is twice as long as the federal marketplace, giving consumers more time to shop for the best health coverage for themselves and their families.

New York has recently introduced a new insurance program for lower-income state residents that don’t qualify for Medicaid or the Child Health Plus Program. It is called the New York State Essential Plan. There are a total of 4 essential plan options and each option is based on your household income level. Two of those options include dental and vision coverage while the remaining two options offer you the opportunity to purchase dental and vision coverage as a rider. Monthly premiums range from $0 to $46 per month.

New York State (NYS) created this program to fill the coverage gap that many individuals and families have as they do not qualify for Medicaid but cannot afford full premium coverage.

Are You Eligible for the Essential Plan?

There are three qualifying elements for you to be eligible for the NY Essential Plan. They are:

Income requirements

Residency and Immigration Status

Aging In and Aging Out

Essential Plan Family Size & Income Eligibility

Household Size

Maximum Annual Income

1*

$25,760

2

$34,840

3

$43,920

4**

$53,000

* Updated April 2021(150% to 200% FPL).

** Add $8,280 for each additional member of your family

Essential Plan 1 premiums are $20 per person per month and Essential Plan 2 costs $0, yet plan benefits are generous and provide you the ten essential health benefits mandated by the Affordable Care Act. Following are the different variations of the NYS Essential Plan:

Essential Plan 1 – Individuals with income greater than 150% and less than or equal to 200% of the FPL.

Essential Plan 2 – Individuals with income greater than 138% and less than or equal to 150% of the FPL.

Essential Plan 3 – Individuals with income equal to or greater than 100% and less than or equal to 138% of the FPL and not eligible for Medicaid due to immigration status.

Essential Plan 4 – Individuals with income below 100% of the FPL and not eligible for Medicaid due to immigration status.

CLICK ABOVE: How to Select a Broker on NYS of Health marketplace

The Essential plan is a cost effective NYS health insurance plan available to those who earn too much to qualify for Medicaid, while providing all of the essential health benefits required by law. All year enrollment. Deadline is the 15th of the respective month.

We have been informed that the NY DFS has recently approved the following measures in the process of CareConnect exiting the market:

For individuals the market exit date is 12/31/2017.

For Small Group the market exit date is 11/30/2017.

All groups renewing starting 12/1/17 will no longer be accepted. Currently active group business will end on the last day of their policy year (For example, a 9/1/17 effective will remain in force until 8/31/18).

With recent announcement “CareConnect Withdraws from NYS Market” a Healthfirst addition to the NY Small Business market is especially important. In many instances the Healthfirst plans have a more robust network than CareConnect for NYC and LI. Namely, they have the same hospitals North Shore LIJ(Northwell), Maimonides, but additionally key hospitals such as Mt. Sinai, NYU, Lenox Hill + urgent cares such as CityMD and GO-Health. Rates are approximately $100/month higher for singles for example than CareConnect and would not be an automatic decision to move to Healthfirst.

Healthfirst has released affordable new 2018 plans for NY small businesses and not a moment too soon. With the recent exit of popular CareConnect of NY the market is starving for an affordable option.

About HealthFirst

Healthfirst had entered the small business market Jan 1, 2017. Healthfirst is a provider-sponsored health insurance company that serves more than 1.2 million members in downstate New York and Nassau county. Healthfirst offers top-quality Medicaid, Medicare Advantage, Child Health Plus, and Managed Long Term Care plans. Healthfirst Leaf Qualified Health Plans and the Healthfirst Essential Plan are offered on NY State of Health, The Official Health Plan Marketplace. Healthfirst offers Healthfirst Pro and Pro Plus, Exclusive Provider Organization (EPO) plans for small-business owners and their employees, and Healthfirst Total, an EPO for individuals.

The Healthfirst options include four Pro EPO plans with comprehensive benefits and pediatric dental and vision coverage that span all the metal tiers (Bronze, Silver, Gold, and Platinum). With Healthfirst plans, employees will have access to key features, including preventive and wellness visits (including annual checkups, vaccinations, and mammograms); a multilin

gual member services team; access to telemedicine via Teladoc; a robust choice of in-network doctors, specialists, hospitals, and urgent care centers; behavioral health and substance abuse services; coverage for acupuncture visits; and a user-friendly member portal that enables members to proactively manage their care.

Value

Healthifrst’s new January 2018 rates are in fact virtually the same as 4thQ 2017. Example, a single rate is approximately $2-$3 higher. Today’s largest networks with popular in-network only GOLD are priced at $857/single monthly. By comparison the Healthfirst Gold plan is $717 annualy or 15% less expensive. For platinum the price gap jumps are even higher – $1050/single vs $850/single.

Members have access to a broad network of providers and dozens of industry-leading hospitals.

Community locations throughout New York City, Long Island and parts of Westchester.

All Metal Levels will be included for all size groups including 1-99 market. Referral’s are not needed to vsisit a Specialist MD but one must select a Primary Care Physician on the enrollment form.

Healthfirst has released affordable new 2018 plans for NY small businesses and not a moment too soon. With the recent exit of popular CareConnect of NY the market is starving for an affordable option.

About HealthFirst

Healthfirst had entered the small business market Jan 1, 2017. Healthfirst is a provider-sponsored health insurance company that serves more than 1.2 million members in downstate New York and Nassau county. Healthfirst offers top-quality Medicaid, Medicare Advantage, Child Health Plus, and Managed Long Term Care plans. Healthfirst Leaf Qualified Health Plans and the Healthfirst Essential Plan are offered on NY State of Health, The Official Health Plan Marketplace. Healthfirst offers Healthfirst Pro and Pro Plus, Exclusive Provider Organization (EPO) plans for small-business owners and their employees, and Healthfirst Total, an EPO for individuals.

The Healthfirst options include four Pro EPO plans with comprehensive benefits and pediatric dental and vision coverage that span all the metal tiers (Bronze, Silver, Gold, and Platinum). With Healthfirst plans, employees will have access to key features, including preventive and wellness visits (including annual checkups, vaccinations, and mammograms); a multilin

gual member services team; access to telemedicine via Teladoc; a robust choice of in-network doctors, specialists, hospitals, and urgent care centers; behavioral health and substance abuse services; coverage for acupuncture visits; and a user-friendly member portal that enables members to proactively manage their care.

Value

Healthifrst’s new January 2018 rates are in fact virtually the same as 4thQ 2017. Example, a single rate is approximately $2-$3 higher. Today’s largest networks with popular in-network only GOLD are priced at $857/single monthly. By comparison the Healthfirst Gold plan is $717 annualy or 15% less expensive. For platinum the price gap jumps are even higher – $1050/single vs $850/single.

Members have access to a broad network of providers and dozens of industry-leading hospitals.

Community locations throughout New York City, Long Island and parts of Westchester.

All Metal Levels will be included for all size groups including 1-99 market. Referral’s are not needed to vsisit a Specialist MD but one must select a Primary Care Physician on the enrollment form.

Attention CareConnect Clients:

Join us for Oct 25th Webinar.

We have been informed that the NY DFS has recently approved the following measures in the process of CareConnect exiting the market:

For individuals the market exit date is 12/31/2017.

For Small Group the market exit date is 11/30/2017.

All groups renewing starting 12/1/17 will no longer be accepted. Currently active group business will end on the last day of their policy year (For example, a 9/1/17 effective will remain in force until 8/31/18).

With recent announcement “CareConnect Withdraws from NYS Market” a Healthfirst addition to the NY Small Business market is especially important. In many instances the Healthfirst plans have a more robust network than CareConnect for NYC and LI. Namely, they have the same hospitals North Shore LIJ(Northwell), Maimonides, but additionally key hospitals such as Mt. Sinai, NYU, Lenox Hill + urgent cares such as CityMD and GO-Health. Rates are approximately $100/month higher for singles for example than CareConnect and would not be an automatic decision to move to Healthfirst.

HealthPass New York, a private health insurance exchange for small businesses, announces that it will offer Healthfirst insurance plans to small business employers in the metropolitan New York City area. Healthfirst, a provider-sponsored health plan serving more than 1.2 million members in New York City and on Long Island, offers small employer group EPO plans to fit the needs of hardworking New Yorkers.

HealthPass will offer Healthfirst Pro EPO plans to eligible employers that employ between one to 100 employees. These plans are available to small businesses with employees who live, work, or reside in New York City and Nassau County. Eligible employers and their employees can begin enrolling in the Healthfirst plans now for coverage that would take effect as early as December 1, 2017.

The Healthfirst options include four Pro EPO plans with comprehensive benefits and pediatric dental and vision coverage that span all the metal tiers (Bronze, Silver, Gold, and Platinum). With Healthfirst plans, employees will have access to key features, including preventive and wellness visits (including annual checkups, vaccinations, and mammograms); a multilingual member services team; access to telemedicine via Teladoc; a robust choice of in-network doctors, specialists, hospitals, and urgent care centers; behavioral health and substance abuse services; coverage for acupuncture visits; and a user-friendly member portal that enables members to proactively manage their care.

About HealthFirst

Healthfirst had entered the small business market Jan 1, 2017. Healthfirst is a provider-sponsored health insurance company that serves more than 1.2 million members in downstate New York and Nassau county. Healthfirst offers top-quality Medicaid, Medicare Advantage, Child Health Plus, and Managed Long Term Care plans. Healthfirst Leaf Qualified Health Plans and the Healthfirst Essential Plan are offered on NY State of Health, The Official Health Plan Marketplace. Healthfirst offers Healthfirst Pro and Pro Plus, Exclusive Provider Organization (EPO) plans for small-business owners and their employees, and Healthfirst Total, an EPO for individuals.

Attention CareConnect Clients:

With recent announcement “CareConnect Withdraws from NYS Market” a Healthfirst addition is especially important. In many instances the Healthfirst plans have a more robust network than CareConnect for NYC and LI. Namely, they have the same hospitals North Shore LIJ(Northwell), Maimonides, but additionally key hospitals such as Mt. Sinai, NYU, Lenox Hill + urgent cares such as CityMD and GO-Health. Rates are approximately $100/month higher for singles for example than CareConnect and would not be an automatic decision to move to Healthfirst.

CareConnect today has announced their intent to withdraw from the NYS 2018 market. The ACA Risk Adjustment Program was penalizing CareConnect again $100 Million for 2018 after a $112 million tax in 2017.

The problems CareConnect was facing were not new and was covered in last month blog. This problem has bipartisan recognition and Cuomo Administration Asks Feds for ‘Immediate Changes’ to Risk Adjustment Program. While this tax or “risk adjustment penalty” was intended to increase competition it is blamed as the single largest bankruptcy cause for the 12 of 16 Obamacare Co-Ops such as the Health Republic of NY and for start-ups like Oscar and CareConnect.

The formula used to calculate payments in the risk-adjustment program has been criticized for unfairly favoring larger plans with more claims experience. Smaller companies that sell on the ACA’s exchanges have said they don’t have as many claims data, and therefore their membership base looks healthier than it is. In a twisted way, the young companies in need of help were actually subsidizing mature Insurers with legacy data systems.

Who is CareConnect?

CareConnect is a physician/hospital-owned Insurer by Northwell Health also formerly known as North SHore LIJ. Careconnect manages the health of 400,000 individuals, including 125,000 customers. Outside of the risk adjustment penalty the Insurer was managing population health and would have posted a profit. Their past rate increases were single digits.

Sadly, this is a tremendous consumer market hit. Their growth was predicated on delivering excellence of care while still mindful of consumer affordability, see chart below. Not only were they on average 20-30% less expensive but their benefits were typically enhanced. Example: A Tradition Gold plan member would NOT have a deductible nor coinsurance for surgeries and hospital stays at a time when all competing Gold plans did.

Regrettably, no State appeal has been victorious as of yet. With logger-head federal conflicts in Government today on repairing Obamacare flaws the victims will once again be the middle-class consumer.

On occasion, there are questions about what a specific word or term means in the context of health

insurance. This glossary is intended to serve as a tool to assist you in understanding some of the

most common terms. A Affordable Care Act (ACA): The comprehensive health care reform law enacted in March 2010. Affordable Coverage: An employer-sponsored health plan covering only the employee, the cost of which

does not exceed a set annual percentage of the employee’s household income. Click here for more

information. Allowed Amount: The maximum amount a plan will pay for a covered health care service. If a provider

charges more than the plan’s allowed amount, the plan participant may have to pay the difference through

a process called balance billing. Annual Limit: A cap on the benefits an insurance company will pay in a year while a plan participant is

enrolled in a particular health insurance plan. Annual limits are sometimes placed on particular services such

as prescriptions or hospitalizations, on the dollar amount of covered services, or on the number of visits that

will be covered for a particular service. After an annual limit is reached, the plan participant must pay all

associated health care costs for the rest of the year. B Balance Billing: When a provider bills a patient for the difference between the provider’s charge and the

patient’s insurance plan’s allowed amount. For example, if the provider’s charge is $100 and the patient’s

insurance plan’s allowed amount is $70, the provider might bill the patient for the remaining $30. Brand-Name Drug: A drug sold by a drug company under a specific name or trademark and that is

protected by a patent. Brand-name drugs may be available by prescription or over the counter. C CHIP (Children’s Health Insurance Program): Insurance program that provides low-cost health coverage to

children in families that earn too much money to qualify for Medicaid, but not enough money to buy private

insurance. Claim: A request for payment of a benefit by a plan participant or his or her health care provider to the

insurer for items or services the participant believes are covered by the plan. COBRA (Consolidated Omnibus Budget Reconciliation Act): A federal law that may allow a plan participant

or his or her dependents to temporarily keep their existing health coverage after certain qualifying events

(such as the participant’s employment ending or losing coverage as a dependent of a covered

employee). Click here for more information. Coinsurance: The percentage of costs of a covered health care service the participant pays after having

paid his or her deductible. Co-op Plan: A health plan offered by a non-profit organization in which the same people who own the

company are insured by the company. Copay (also known as copayment): A fixed amount the participant pays for a covered health care service

after having paid his or her deductible. Coverage:See Health Insurance Cost Sharing: The share of costs covered by insurance that a plan participant pays out of his or her own

pocket. Cost sharing generally includes deductibles, coinsurance, and copays, but does not include

premiums. D Deductible: The amount a plan participant pays for covered health care services before his or her insurance

plan starts to pay. Dental Coverage: Benefits that help pay for the cost of visits to a dentist. Dependent: A child or other individual for whom a parent, relative, or other person may claim a personal

exemption that reduces their tax obligation. Diagnostic Test: Test to figure out what the plan participant’s health problem is. For example, an x-ray can be

a diagnostic test to diagnose a broken bone. Disability: A limit in a range of major life activities. This includes activities like seeing, hearing, and walking, and

tasks such as thinking and working. Drug List: See Formulary. E Emergency Medical Condition: An illness, injury, symptom (including severe pain), or condition severe enough

that a reasonable person would seek medical attention right away. Emergency Medical Transportation: Ambulance services for an emergency medical condition. Emergency Services: Services to check for or treat an emergency medical condition. Employer Mandate: Provision of the Affordable Care Act that requires certain employers with at least 50 full-

time employees (including full-time equivalents) to offer health insurance coverage to their full-time

employees (and their dependents) that meets certain affordability and minimum value standards, or pay a

penalty tax. The employer mandate is often referred to as “pay or play.” Click here for more information. Employer Shared Responsibility Provision: See Employer Mandate. Essential Health Benefits: A set of 10 categories of services health insurance plans must cover under

the Affordable Care Act. These include doctors’ services, inpatient and outpatient hospital care, prescription

drug coverage, pregnancy and childbirth, mental health services, and more. Click here for more information. Exchange: See Health Insurance Marketplace. Excluded Services: Health care services that a plan does not pay for or cover. F Flexible Spending Arrangement (FSA): See Health Flexible Spending Arrangement. Formulary: A list of prescription drugs covered by a prescription drug plan or another insurance plan offering

prescription drug benefits. A formulary is also often called a drug list. Fully Insured Plan: A health plan purchased by an employer from an insurance company. G Generic Drug: A drug that has the same active-ingredient formula as a brand-name drug. Grandfathered Health Plan: A group health plan that was created—or an individual health insurance

policy that was purchased—on or before March 23, 2010. Grandfathered health plans are exempted from

many changes required under the Affordable Care Act. Plans or policies may lose their “grandfathered”

status if they make certain significant changes that reduce benefits or increase costs to consumers. A health

plan must disclose in its plan materials whether it considers itself to be a grandfathered plan and must also

provide consumers with contact information for questions or complaints. Group Health Plan: In general, a health plan offered by an employer or employee organization that provides

health coverage to employees and their families. H Health Care Provider: An individual or facility that provides health care services. Examples include a doctor,

nurse, chiropractor, physician assistant, hospital, surgical center, skilled nursing facility, and rehabilitation center. Health Flexible Spending Arrangement (Health FSA): An arrangement an individual establishes through his or

her employer to pay for out-of-pocket medical expenses with tax-free dollars. These expenses include

insurance copays and deductibles, and qualified prescription drugs, insulin, and medical devices.

Contributions to an FSA are subject to an annual limit that is adjusted for inflation each year. These

arrangements are also referred to as Health Flexible Spending Accounts. Health Insurance: A contract that requires a health insurance company to pay some or all of a plan

participant’s health care costs in exchange for a premium. Health Insurance Marketplace: A service that helps people shop for and enroll in health insurance. The

federal government operates the Marketplace, available at HealthCare.gov, for most states. Some states run

their own Health Insurance Marketplaces. Health Maintenance Organization (HMO): A type of health insurance plan that usually limits coverage to care

from doctors who work for or contract with the HMO. There are generally two main types of HMOs:

Traditional HMO: This type of HMO provides no benefits for services obtained outside of a network.

Open-Access HMO: This type of HMO allows enrollees to receive services from an out-of-

network provider at a higher cost than the enrollee would pay at an in-network provider. The

additional costs may be in the form of higher deductibles, copays, or coinsurance.

Health Reimbursement Arrangement (HRA): Employer-funded group health plans from which employees are

reimbursed tax-free for qualified medical expenses up to a fixed dollar amount per year. Unused amounts

may be rolled over to be used in subsequent years. Also referred to as a Health Reimbursement Account. Health Savings Account (HSA): A type of savings account that allows an individual to set aside money on a

pre-tax basis to pay for qualified medical expenses, if he or she has a high deductible health plan. HSA

contributions are subject to an annual limit that is adjusted for inflation each year. High Deductible Health Plan (HDHP): A plan with a higher deductible than a traditional insurance plan. To be

considered an HDHP, the plan must meet minimum deductible and maximum out-of-pocket limit

requirements, which are annually adjusted for inflation. High-Risk Pool Plan: A state-subsidized health plan that provides coverage for individuals with expensive pre-

existing health care conditions. Home Health Care: Health care services and supplies an individual receives in his or her home under doctor’s

orders. Services may be provided by nurses, therapists, social workers, or other licensed health care providers. Hospice Services: Services to provide comfort and support for persons in the last stages of a terminal illness.

Hospitalization: Care in a hospital that requires admission as an inpatient and usually requires an overnight stay. I Individual Health Insurance Policy: Insurance policy for an individual who is not covered under an employer-

sponsored plan. Individual Mandate: Provision of the Affordable Care Act that requires every individual to have minimum

essential coverage for each month, qualify for an exemption, or make a penalty payment when filing his or

her federal income tax return. Individual Shared Responsibility Provision: See Individual Mandate. In-Network: Health care providers (e.g., specialists, hospitals, laboratories) that have accepted contracted

rates with the insurer in order to participate in the insurer’s network. The insured person typically pays a lower

price for using services within the network. Inpatient Care: Health care that an individual receives when formally admitted as a patient to a health care

facility, like a hospital or skilled nursing facility. Internal Limit: Limitation that applies to individual categories of care—for example, a $250-per-

procedure deductible for inpatient surgery. L Lifetime Limit: A cap on the total lifetime benefits a plan participant may receive from his or her insurance

company. After a lifetime limit is reached, the insurance plan will no longer pay for covered services. M Mail-Order Drugs: Drugs that can be ordered through the mail. Marketplace: See Health Insurance Marketplace. Medicaid: A joint state and federal insurance program that provides free or low-cost health coverage to

some low-income people, families, children, pregnant women, the elderly, and people with disabilities. Medical Care: Services rendered by a hospital or qualified medical care provider. Medical Loss Ratio (MLR): A basic financial measurement used in the Affordable Care Act to encourage

health plans to provide value to enrollees. If an insurer uses 80 cents out of every premium dollar to pay its

customers’ medical claims and activities that improve the quality of care, the company has a medical loss

ratio of 80%. A medical loss ratio of 80% indicates that the insurer is using the remaining 20 cents of each

premium dollar to pay overhead expenses, such as marketing, profits, salaries, administrative costs, and

agent commissions. The Affordable Care Act sets minimum medical loss ratios for different markets, as do

some state laws. Medicare: A federal health insurance program for people aged 65 and older, certain younger people with

disabilities, and people with End-Stage Renal Disease (permanent kidney failure requiring dialysis or a

transplant, sometimes called ESRD). Medicare consists of four parts:

Medicare PartA: Covers hospital, skilled nursing, nursing home, hospice, and home health services care.

Medicare PartB: Covers medically necessary and preventive services.

Medicare PartC (Medicare Advantage): A type of Medicare health plan offered by a private

company that contracts with Medicare to provide the beneficiary with all of his or her Part A and Part B

benefits.

Medicare PartD: A program that helps pay for prescription drugs for people with Medicare who join a

plan that includes Medicare prescription drug coverage. There are two ways to get Medicare

prescription drug coverage: through a Medicare Prescription Drug Plan or a Medicare Advantage Plan

that includes drug coverage, both of which are offered by insurance companies and other private

companies approved by Medicare.

Minimum Essential Coverage (MEC): Any insurance plan that meets the Affordable Care Act requirement for

having health coverage (sometimes called qualifying health coverage). Individuals without minimum

essential coverage may be subject to the individual mandate penalty. Minimum Value: A standard of minimum coverage that applies to employer-sponsored health plans. Click here for more information. N Network: The facilities, providers, and suppliers a health insurer or plan has contracted with to provide health

care services. O Obamacare: See Affordable Care Act. Open-Access HMO: A type of HMO that allows enrollees to receive services from an out-of-network provider

at a higher cost than the enrollee would pay at an in-network provider. The additional costs may be in the

form of higher deductibles, copays, or coinsurance. Open Enrollment Period: The yearly period when people can enroll in a health insurance plan.

Out-of-Network: Services received outside an insurer’s network. These services typically carry a higher cost to

the insured person. Out-of-Pocket Costs: Expenses for medical care that are not reimbursed by insurance. Out-of-pocket costs

include deductibles, coinsurance, and copays for covered services, plus all costs for services that are not

covered. Out-of-Pocket Limit: The most a plan participant can be required to pay for covered services in a plan year.

The out-of-pocket limit does not include monthly premium amounts or spending for services the plan does not

cover. An out-of-pocket limit is also often called an “out-of-pocket maximum.” Out-of-Pocket Maximum: See Out-of-Pocket Limit. Outpatient Care: Care received where a doctor has not written an order to admit the individual to a hospital

as an inpatient (in these cases, an individual is an outpatient even if he or she spends the night in the hospital,

but typically it does not require an overnight hospital stay). P “Pay or Play”: See Employer Mandate. Physician Services: Health care services a licensed medical physician provides or coordinates. Plan Year: A 12-month period of benefits coverage under a group health plan. This 12-month period need not

align with the calendar year. Preauthorization: A decision by a health plan that a health care service or product is medically necessary. A

health plan may require preauthorization for certain services before they are provided (except in an

emergency), though preauthorization is not a promise by a health plan to cover the cost. Pre-Existing Condition: A health problem an individual had before the date that his or her new health

coverage starts. Pre-Existing Condition Exclusion Period: The period during which an insurance policy will not pay for care

relating to a pre-existing condition. Preferred Provider Organization (PPO): A type of health plan that contracts with medical providers, such as

hospitals and doctors, to create a network of participating providers. Under a PPO, a plan participant pays

less in out-of-pocket costs if he or she uses providers that belong to the PPO’s network. Premium: The amount a plan participant pays for his or her health insurance every month. Premium Tax Credit: A tax credit an individual can use to lower his or her premium when he or she enrolls in a

plan through the Health Insurance Marketplace. The Premium Tax Credit is based on the income estimate

and household information the individual provides on his or her Health Insurance Marketplace application. Prescription Drugs: Drugs and medications that, by law, require a prescription. Prescription Drug Coverage: A health plan that helps pay for prescription drugs and medications. Preventive Services: Routine health care that includes screenings, check-ups, and patient counseling to

prevent health problems. Primary Care: Health services that cover a range of prevention, wellness, and treatment programs for

common illnesses. Primary Care Provider: A physician, nurse practitioner, clinical nurse specialist, or physician assistant who

provides, coordinates, or helps an individual access a range of primary care services. Q Qualified Health Plan: An insurance plan that is certified by the Health Insurance Marketplace,

provides essential health benefits, follows established limits on cost sharing (like deductibles, copays, and out-

of-pocket limits), and meets other requirements under the Affordable Care Act. All qualified health plans

meet the minimum essential coverage requirement. R Referral: A written order from a primary care provider directing a patient to see a specialist or receive certain

health care services. Under many health plans, a plan participant must obtain a referral before he or she can

receive health care services from anyone except his or her primary care provider. Rehabilitation Services: Health care services that help an individual keep, get back, or improve skills and

functioning for daily living that have been lost or impaired because he or she was sick, hurt, or disabled. These

services may include physical and occupational therapy, speech therapy, and psychiatric rehabilitation

services in a variety of inpatient and outpatient settings. Rescission: The retroactive cancellation of a health insurance policy. Insurance companies will sometimes

retroactively cancel an entire individual health insurance policy if an individual made a mistake on his or her

application for the policy that amounts to fraud or an intentional misrepresentation of material fact. S Screening: A type of preventive service that includes tests or exams to detect the presence of a health issue,

usually performed when an individual has no symptoms, signs, or prevailing medical history of a disease or

condition. Self-Insured Plan: Type of plan, usually present in larger companies, where the employer itself collects

premiums from enrollees and takes on the responsibility of paying employees’ and dependents’ medical

claims. These employers often contract with a third-party administrator for services such as enrollment, claims

processing, and provider networks. Skilled Nursing Care: Services from licensed nurses in an individual’s home or in a nursing home. Special Enrollment Period (SEP): A time outside the yearly Open Enrollment Period when an individual can sign

up for health insurance. An individual typically qualifies for a Special Enrollment Period as a result of certain

life events, such as losing other health coverage, moving, getting married, having a baby, or adopting a

child. By law, employer-sponsored plans must provide a special enrollment period of at least 30 days.

Specialist: A health care provider focusing on a specific area of medicine or group of patients to diagnose,

manage, prevent, or treat certain types of symptoms and conditions. Summary of Benefits and Coverage (SBC): An easy-to-read summary that allows an individual to make

apples-to-apples comparisons of costs and coverage between health plans. An individual most commonly

receives an SBC when he or she shops for coverage or renews or changes coverage. T Traditional HMO: A type of HMO that provides no benefits for services obtained outside of a network.

TRICARE: A health care program for active-duty and retired uniformed service members and their families. U Urgent Care: Care for an illness, injury, or condition serious enough that a reasonable person would seek care

right away, but not so severe that it requires emergency room care. Usual, Customary, and Reasonable Charge (UCR): The amount paid for a medical service in a geographic

area based on what providers in the area usually charge for the same or similar medical service. The UCR

amount is sometimes used to determine the allowed amount. V Vision Coverage: A health benefit that at least partially covers vision care, such as eye exams and glasses. W Waiting Period: The time that must pass before coverage can become effective for an employee or

dependent who is otherwise eligible for coverage under an employer-sponsored health plan. Well-Baby/Well-Child Care: Routine doctor visits for comprehensive preventive health services that occur

when a child is 2 years of age or younger, and annual visits until a child reaches age 21. Services include

physical exams and measurements, vision and hearing screenings, and oral health risk assessments.

It is intended to serve as a tool to assist you in understanding some of the most common terms. Call (855) 667-4621 for more info.

HealthPass New York will start offering OSCAR Health Plans effective Sept 1, 2017 to small employers. Oscar will offer eight plans with varying benefits package with 1 to 100 employees. The plans are available to small businesses located in New York City, Long Island, Westchester and Rockland counties. NJ residents can also access Hospitals & physicians through the NJ Qualcare PPO Network

HealthPass New York, a private insurance exchange for small employers. The addition of Oscar gives small businesses access to 3 health networks – Oxford, CareConnect and Oscar. Also, Guardian is the insurer of record for the ancillary benefits comprising dental, vision, life insurance, disability and accident insurance

Oscar entered the NY market on Jan 1, 2014 and had around 16,000 members. In 2015, it expanded coverage to New Jersey and grew to about 40,000 members. In 2016, Oscar had 145,000 members in New York, New Jersey, California, and Texas. Oscar’s cutting edge technology and pioneering benefits have simplified the consumer health insurance experience propelled easier access and understanding of health plans. Examples of success have been ease of physician locator, online appointment setting and no cost telemedicine 24/7. Additionally, some plans have $0 Copay generics and annual 3 free office visits

Why a Private Exchange? The advantage of a Private Exchange is the ability to empower employees with choice. Much like a 401K your employees can use a defined contribution allocation for benefits. As affordable health plan networks are increasingly smaller with specific coverage areas the one size show for all approach to benefits no longer works.

If you’re a small business owner who has concerns about payroll, filing paperwork, and complying with government regulations, co-employment may be the service you’ve been looking for. In some cases, a Private Exchange may NOT be right for you. With Health Care Reform your company may qualify for a small business tax credit or a be eligible for a large group discount under a PEO.

Try us on a custom demo, contact us at (855)667-4621.

insurance companies and providers — so patients are clear on what their plan covers — ensures patients aren’t responsible for excess costs, and establishes an arbitration process to resolve payment disputes between providers and insurers, a mechanism intended to better control costs.

insurance companies and providers — so patients are clear on what their plan covers — ensures patients aren’t responsible for excess costs, and establishes an arbitration process to resolve payment disputes between providers and insurers, a mechanism intended to better control costs.