The Google of health insurance?Oscar entered the NY market on Jan 1, 2014 and had around 16,000 members. In 2015, it expanded coverage to New Jersey and grew to about 40,000 members. In 2016, Oscar had 145,000 members in New York, New Jersey, California, and Texas. Oscar’s cutting edge technology and pioneering benefits have simplified the consumer health insurance experience propelled easier access and understanding of health plans. Examples of success have been ease of physician locator, online appointment setting and no cost telemedicine 24/7. Additionally, some plans have $0 Copay generics and annual 3 free office visits

The Numbers:

NY based with 900+ employees

260,000 members across 6 states

$890M raised from top investors (Fidelity, Goldman Sachs, Google, etc.)

$375M investment from Alphabet Inc. (Google parent company)

After doubling footprint for 2018,Oscar is on-track for 3x growth

Oscar Member Engagement:

27% of Oscar members utilize DocOnCall vs. industry average of 3%

35% of first time doctor appointments start with Oscar

3x customer satisfaction score vs. the industry average

48% of all Oscar members use the Oscar app, compared to 7% of other health insurance carriers

Doctor on Call has led to approximately $600 in savings per member

Concierge Team has led to an approx. $3,600 in savings in member OON claims

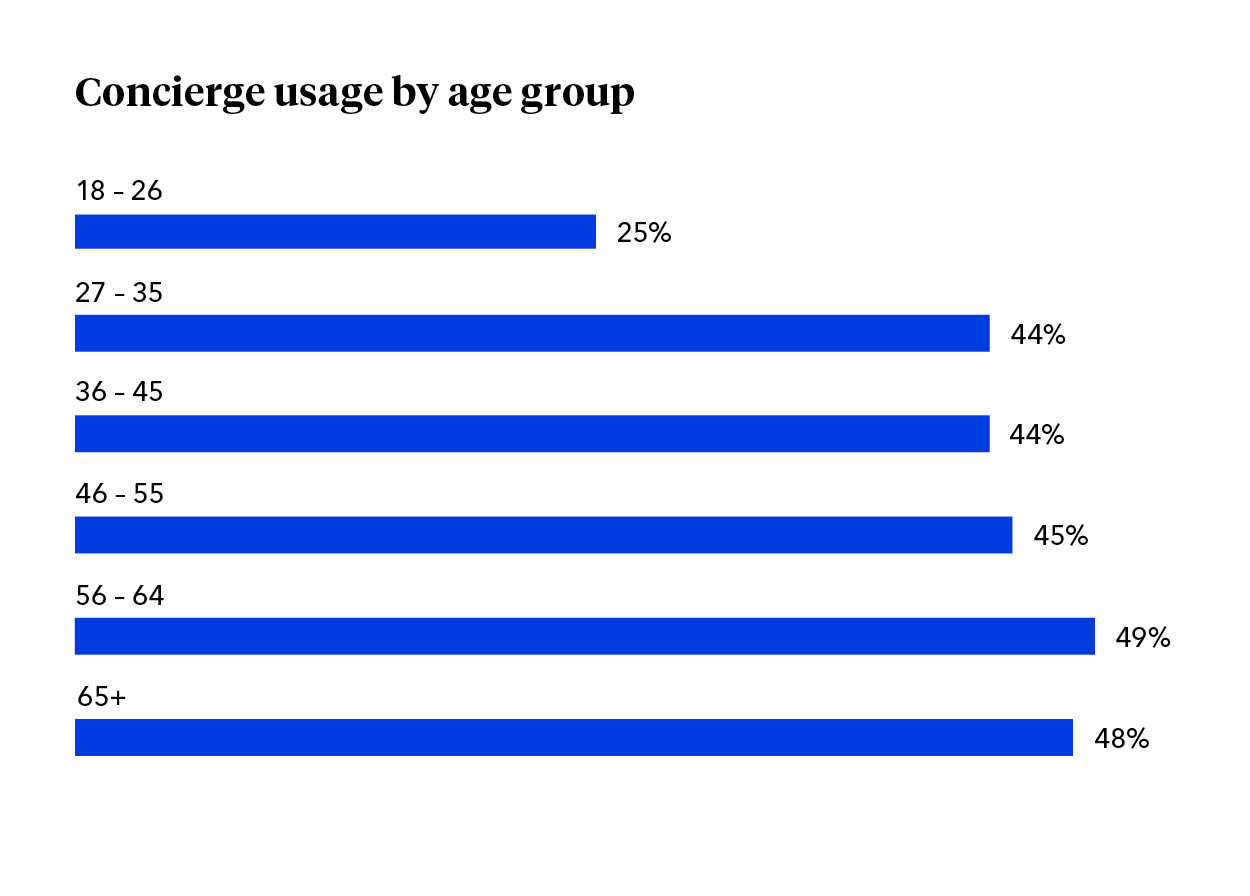

Pre-medicare population almost 2x Concierge Team utilization vs. the “younger” demographic

The Oscar Member Experience

Concierge Service: Every member is placed on a team of 5 care guides and 1 nurse that help members achieve better health outcomes and lower costs.

Doctor on Call: 24/7, free and unlimited telemedicine that works nationwide. This is a great way to care of basic primary care at the member’s convenience

New Oscar 2019

Oscar’s current network will be rebranded as Circle Network

15 plans across 4 metal tiers

NEWCircle Plus Network include:

Northwell (formerly North Shore LIJ)

Memorial Sloan-Kettering

Multiplan National Network for out of state

Westchester Expansion – Northern Westchester Hospital (Mt. Kisko), Phelps Hospital (Tarrytown) and the Westmed Medical Gorup added.

NEW: Only $0 deductible required Silver Plans!

Transitioning before 2019. Groups enrolling 11/1/19 can upgrade 1/1/19 to Circle Plus Network

NYS has approved 2019 Final Rates last Friday. Small group rates will increase 3.8% and 8.6% for individuals.

As per NY State Law, Health Insurers are required to send out early notices of rate request filings to groups and subscribers see original –NYS 2019 Rate Requests. Despite only 3 months of mature claims data experience for 2018 health insurers’ original requests were noticeably below average 7.5% for small group and 24% for individuals. Ultimately NYS reduced this request substantially by approximately 50%.

Experts are concerned over the long term effects. Example, the Individual mandate was removed last December by Presidential order. Without the Mandate anyone can drop insurance without penalty. A comparable take away for similar auto insurance industry would be something like this -Drivers ought not be mandated to buy auto insurance as its a profit scheme by Insurers. While a popular decision this will hardly bend the curve long term and reduce competition. Furthermore, the new order of Selling Across State lines makes NYS most unwelcoming.

OTHER STATES

Insurers have been filing to sell Obamacare plans that will go into effect in 2019, and in some states they appear to be pricing in for the fact that the mandate is going away next year. Other states are seeing mild increases, but that is in part because they saw significant hikes for the previous year.

Insurers have concluded that fewer people will enroll without the mandate than otherwise, so in some places they are pricing their plans higher based on the assumption that sicker people will be left behind, which will increase medical costs for those left. It is well worth pointing out that in recent years the loss federal risk reinsurance corridor funds account for 5.5 percent of the rate increase.

How are neighboring States doing?

In NJ, not that bad. Last year the average increase were 5.5% for small groups and some popular plans such as Horizon Blue Cross Blue Shield’s OMINA increasing only 4.8% increase. This year the increase is only 5.2. Other insurers offering EPO and HMO plans in the individual market for 2019 include Oscar Health and Oxford Health Plans.

With individual mandate repeal fewer people will buy health insurance raising the prices for those who do. NJ Banking and Insurance Department officials said premium prices would have increased, on average, by 12.6 percent.

For CT market, on the other hand, things are much worse at least for the individual marketplace with average 25% rate increases last year. The 2019 proposed rate increases for both the individual and small group market are, on average lower, than last year: The proposed average small group rate increase request is a 10.22 percent and ranges from -5.0 percent to 21.1 percent. This compares to the average increase request of 18.06 percent requested last year.The proposed average individual rate increase request is 12.3 percent and ranges from -10.9 percent to 31.0 percent. This compares to the average increase request of 25.51 percent requested last year.

Final plan rates in New Jersey & CT will be finalized and released in the fall, state officials said. ACA open enrollment begins Nov. 1

Trend: Trend is a factor that accounts for rising health care costs, including the cost of prescription drugs, and the increased demand for medical services.

Uncertainty in Washington:

Removal of penalty for individual mandate: The elimination of the penalty means that individuals who are typically younger and healthier would have no inducement to participate in the insurance pool, which could further destabilize the market. Lack of participation shrinks the pool and increases the cost of insurance to the remaining members.

Short-duration health plans and Association Health Plans: Still pending are final federal regulations on non-ACA compliant short-duration plans, which may have implications for the ACA risk pool. Also, Connecticut along with other state insurance regulators, are awaiting clarification from the federal government on new federal regulations allowing association health plans, which could further shrink the ACA risk pool.

A bipartisan group of congressional representatives has discussed an agreement to extend and guarantee the payments, but it’s unclear whether they could do so by the new filing deadline of Sept. 5. A lawsuit filed by Congress against the Obama administration to challenge the payments is still pending. In addition, Trump has repeatedly threatened to withhold payments to insurers that reduce cost-sharing – deductibles, copays and coinsurance – paid by low-income customers. More than half of New Jersey’s marketplace customers receive that assistance, and without it, most would be unable to afford coverage.

Finally, a tax on health insurance premiums has been reinstated in 2018 after a one-year “tax holiday” approved by Congress for 2017. That contributed 2.3 percent to the rate hikes that insurers requested for 2019 and for 2019

SMALL GROUP MARKET VS. INDIVIDUAL MARKET

Importantly, small group market is still more advantageous than individual markets unless one gets a sizable low-income tax credit. Overall, about 350,000 individual plan consumers will be affected by the price hike, while more than a million users will be hit by higher small group fees. Last year, Blue Cross Blue Shield released a study showing Obamacare user costs were 22 percent higher than people with employer-sponsored health plans, while UnitedHealthplans to exit most Exchanges see – Breaking: Oxford Exits Metro Indiv & Oxford Liberty HMO 2017.

The correct approach for a small business in keeping with simplicity is a Private Exchange and with our large buying group PEO partnerships. This is a true defined contribution empowering employees with a choice of leading insurers offering paperless technologies integrating HRIS/Benefits/Payroll. Both employee and employers still gain tax advantage benefits under the business. Also, the benefits, rates and network size are superior under a group plan as the risk are lower for small group plans than individual markets.

Learn how a Private Exchange and our PEO Partnership can help your group please contact us at info@medicalsolutionscorp.com or (855)667-4621.

Survey Shows 94% of PEOs Expect an Increase in Employees

Businessman pressing a People concept button.

Professional Employer Organizations (PEO) growth doesn’t appear to be slowing down. Earlier this year, NAPEO released the results from there 2017 Q3 Industry Pulse Survey. The findings showed that PEOs are continuing to grow, and at an impressive pace. In the report, 72% of PEOs reported revenue growth in Q3 of 2017, compared to Q3 of 2016.

With all that is happening with employment laws, healthcare and health insurance, and other areas of HR that impact small and medium-sized businesses (SMBs), it is easy to see why PEOs and other HR outsourcing options are seeing, in many cases, rapid industry growth.

Now, NAPEOs latest Quarterly Pulse Survey, which compared the 4th quarter of 2017 to the 4th quarter of 2016, shows that PEO growth is still occurring, and will almost certainly continue in 2018 and beyond.

DATA FROM THE 2017 Q4 NAPEO PULSE SURVEY

The NAPEO Quarterly Pulse Survey – Q4 2017 was conducted in early 2018, and was taken by 32 PEO executives.

The first result from the survey looked at PEO revenue. 71.9% of PEO executives said their organization’s revenue increased in Q4 of 2017, compared to Q4 of 2016.

Broken down further, 50% said that revenue increased somewhat, and 21.9% said revenue increased significantly.

Next, the survey showed that PEOs experienced an increase in the average annual wage per worksite employee (WSE), with 65.5% of executives responding.

NAPEO’s findings also revealed that 66% of PEOs saw an increase in gross profit. Of this 66%, 43.3% said gross profit increased somewhat, while 23.3% said it increased significantly.

OPERATING INCOME, NUMBER OF CLIENTS, AND WSE PROJECTION DATA

The next group of results from the survey uncovered data around operating income, the number of clients, and worksite employee projection information.

First, the report showed that 65.7% of PEO executives reported an increase in operating income in the 4th quarter of 2017, compared to the 4th quarter of 2016. The 65.7% can be broken down further, with 43.8% saying that operating income increased somewhat, and 21.9% increasing significantly.

Next, 59.4% of PEOs said that the number of clients increased, while 31.3% said that the number of clients stayed about the same. Of the 59.4%, 50% said that clients increased somewhat, and 9.4% said clients increased significantly.

Lastly, the survey asked PEO executives about worksite employee (WSE) projections over the next 12 months.

Perhaps the most promising and impressive statistic found in the quarterly survey, almost 94% expect WSEs to increase. Here is the full breakdown:

71% expect EE to increase somewhat

22.6% expect EE to increase significantly

3.2% expect EE to stay about the same

3.2% expect EE to decrease somewhat

With PEOs seeing an increase in revenue throughout 2017, and executives overwhelmingly expecting EE to increase over the next 12 months, revenue outlooks for the rest of 2018 and into 2019 look extremely promising throughout the PEO industry.

PROFESSIONAL EMPLOYER ORGANIZATIONS CONTINUE TO THRIVE

Much like the last few Quarterly Pulse Surveys from NAPEO, the 2017 Q4 survey shows that despite all of the uncertainty and complexity with various areas of HR, PEOs continue to grow.

Regarding the survey, Pat Cleary, President & CEO of NAPEO, said, “This is just the latest example that more and more business owners are realizing the true value of using a PEO. Surveys and studies consistently show that using a PEO is good for a business and its employees. PEOs provide a real benefit to businesses by providing HR services and solutions that they would otherwise be unable to afford.”

Some additional findings from the survey include:

Average annual wage per WSE increased somewhat

Average number of WSEs per client company stayed about the same

Number of internal employees (including salespeople) stayed about the same

Number of Worker’s Compensation claims reported to carrier stayed about the same

The survey also revealed that the average PEO has 19 worksite employees per client.

Learn how a PEO can help grow your business. Check out PEO Case Studies here and learn how they can apply to you.

Click below for a free PEO assessment. OurPEO Quoting Tool ensures that we have first-hand insight as to what the small business owner needs to be successful.

Professional Services: New York Law Firm’s Benefit Benchmark Study Reveals Gap In Offerings

A law firm with a benefit offering below the New York law firm benchmark, no HR person on staff, no formal recruitment strategy and no employee development plan was struggling to attract top lawyers and paralegals, and to keep top producers. This was affecting their stability, employee morale, and ultimately, their bottom line. After losing one of their highest billing attorneys and a key associate to a larger firm with more robust benefit offerings, they realized they needed to make an immediate and drastic change to recruit and retain quality employees.

SOLUTION

Our PEO partner immediately assigned a seasoned Human Resources Manager with vast experience working with law firms to help, and conducted a market analysis of other firms in the area. After establishing a benchmark, the PEO developed an innovative employee benefits program that rivals top law firms in the area. Our PEO partner then devised a recruitment and retention strategy designed to reposition the firm in the marketplace.

RESULT

The firm now offers benefits and employee development that are on par with their top competitors. They have a clear plan on how to increase employee satisfaction and retain quality people while attracting top new talent. Their turnover has reduced significantly, and employees shared positive feedback during and after their benefit enrollment meetings via employee satisfaction and engagement surveys. Leadership can now focus on clients and on growing the firm.

Click below for a free PEO assessment. OurPEO Quoting Tool ensures that we have first-hand insight as to what the small business owner needs to be successful.

Contact Us Now Learn how our Agency is helping buinsesses thrive in today’s economy. Please contact us at info@medicalsolutionscorp.com or (855)667-4621.

By Thomas J. Donahue, President and CEO, U.S. Chamber of Commerce Sept 25 ,2017

Small, Midsize Businesses Hold Key to Growth The U.S. economy grew at a rate of 3% last quarter, the fastest pace in more than two years and a welcome sign of momentum following a sluggish recovery. What do we need to do to ensure this progress continues? For one thing, we need to listen to America’s small and midsize business leaders. These economic playmakers often get drowned out in our modern political discourse, but the U.S. Chamber of Commerce is working to make sure their voices are heard—because our country depends on them.

We’ll never kick our economy into high gear if we don’t understand the concerns and goals of the business leaders who are on the ground working to expand their companies every day. In debates over tax reform, health care, regulations, and more, input from these Americans holds the key to boosting the entire country. After all, two-thirds of new private sector jobs come from our 30 million small and midsize businesses. When we respond appropriately to their frustrations, we end up helping our workers and communities too.

The Chamber conducts surveys of small and midsize businesses every quarter, and we use the results to keep our government in tune with our economy. We also host events such as our recent National Small Business Summit in Washington, D.C., and our Small Business Series of events across the country. Our priority with these is t

o listen and then amplify what we hear.

In the case of our most recent surveys, about 60% of small business leaders in the second-quarter had a positive outlook for their companies and the environment in which they operate. Our third-quarter survey of midmarket business owners, released last week, was slightly less encouraging. These leaders are still optimistic, yet their outlook had dimmed from the previous quarter, partly due to a lack of progress on policy reform in Washington.

These business leaders are eager to hold government accountable. At our recent Small Business Summit, for example, we gave attendees the opportunity to engage directly with members of Congress—and the response was overwhelming. About 200 business owners stormed Capitol Hill to talk tax reform and other issues.

With the third-quarter ending this Saturday, we’ll soon get another official reading on America’s economic performance. The Chamber hopes to see continued momentum with another strong quarter. But regardless of the result, it is clear that small and midsize businesses are ready for real action on vital issues like tax reform and infrastructure. Government leaders would do well to listen up—and get moving.

Contact Us Now Learn how our Agency is helping buinsesses thrive in today’s economy. Please contact us at info@medicalsolutionscorp.com or (855)667-4621.

Learn how SMB are accelerating growth using our PEO Partnerships exclusives:

Are you asking the right questions? Yes, your Broker was referreered by family or friend. You may have met him at golf outing or an event. With rapidly changing laws and markets it maybe a good idea to refer back to this checklist.

To ensure that your broker is the right fit for your company, ask prospective brokers these 10 questions:

What is their method for controlling healthcare costs? The ideal broker will give his or her professional advice to your management and HR teams in order to create a strategy that will work for years. Using data analytics and benchmarking they will be able to show you where your premium falls in comparison to companies similar to yours. Additionally, they will negotiate with carriers to get you the best rate and suggest alternative options for funding your benefits.

What services should I expect? It is important to understand the scope of services that your benefits broker can provide. First, you need to determine what is most important to your company’s needs, then you can discuss what services you will need from your broker in order to have a well-run benefits plan.

Do they have solid references and industry experience? A reliable benefits broker will be able to provide you with references in similar industries and demographics to yours. This guarantees your benefits broker is focused on the specific types of products your employees need.

How will they support your company and your employees? Providing ongoing employee support for benefits-related issues and questions beyond enrollment is important. The best brokers are the ones who are invested in your employees and want them to completely understand their benefit options. You will want to hire a benefits broker who will host informational sessions and schedule employee meetings in order to meet this goal.

What kind of online enrollment and other tools do they offer? Model brokers offer a fully-integrated solution shaped to fit your needs. These brokers will ensure that the technology is equipped to solve your problems. Many brokers offer enterprise class HRMS and Open Enrollment solutions.

How do they plan on handling the renewal process? Typically, the renewal process starts a minimum of 45 to 60 days prior to the renewal date. However, you want a broker who will be proactively working on your plan year-round. This gives both parties involved plenty of time to review the data, gather competitive quotes, and make the right decision. Your broker should negotiate your renewal rate each year and be able to suggest products that would be appealing to your employees.

How do they ensure that their clients are kept in compliance, and what resources do they offer? A good broker takes compliance to the next level. They will supply you with all of the tools and information you need in order to make informed decisions. In addition to communicating compliance information and providing technology to manage compliance issues, their services should include a dedicated contact, representative, or call center that you can use for questions or concerns.

How much support will they offer your HR department? The ideal broker will act as a trusted partner who works strategically with HR, supplying the vital tools for success. Tools such as online enrollment, HRIS software, and human resource outsourcing services. You want your broker to be a total solution provider for your organization.

Will you have a dedicated account manager? As an employer, you want your broker to be accessible in case you ever need them. A dedicated account manager is someone who will always be available to help you if you have a question about your plan or are having trouble making a claim. This contact can help you resolve any issues and answer questions.

How will they determine the best coverage for you? Your employees’ insurance and benefit needs will change over time due to both internal and external causes and changes, so your benefits broker should not only demonstrate the experience to create initial packages, but continue to monitor employee and business needs based on the financial information you provide.

Insurance and benefits offerings are the second largest employee expense outside of payroll. And who is responsible for it all? Your benefits broker. Insurance programs can directly impact employee turnover, retention numbers, workplace productivity, job offer acceptance rates, and candidate quality. With the ability to affect your organization at a very large scale, it is important to have a broker who outperforms the rest. Analyzing these ten critical questions in relation to your organization’s needs will help you make a more informed decision about your benefits broker. If your broker is incapable of answering these questions then odds are you should reconsider.

Contact Us NowLearn how our Agency is helping buinsesses thrive in today’s economy.Please contact our payroll and reimbursement team on your HR/Payroll/Compliance needs at Millennium Medical Solutions Corp at info@medicalsolutionscorp.com or (855)667-4621 for immediate answers.