Last week the House voted the unpopular Obamacare Cadillac Tax to be permanently repealed 419-6. However, much like a bad cold, the Health Insurance Tax (the HIT) is back for 2020. Website Stop The Hit calculates $5,000 as the average tax for a 10 man small business for example.

Who’s affected?

No one escapes the $16 billion HIT. The return of the Health Insurance Tax (HIT) means higher costs and fewer jobs for hardworking Americans. Absent immediate Congressional action to delay the HIT, small businesses and families will face $500 on average in higher premiums for 2020. To make matters worse, the increased cost burden on small businesses from the HIT could result in the U.S. workforce being reduced by 152,000 to 286,000 jobs over a decade. Te HIT is projected to increase premiums for seniors by $241.

How much for 2020?

For Small business, this translates to an estimated 2.5%-3% added surcharge. For States like NYS where there is already approx. 16% added surcharge to high premiums, this becomes daunting. It is no surprise the unpopular HIT was suspended. In 2017, payers escaped making $13.9 billion in payments due to the moratorium, according to a 2018 analysis by Oliver Wyman, commissioned by UnitedHealth Group. This may have saved consumers billions on their insurance coverage.“The taxes on health insurance are non-deductible for federal tax purposes for health insurers,” the report explained.

In some states, such as Vermont, the price of insurance would have more than quadrupled. The payer trade group published a fact sheet on this. “Allowing a tax to resume in 2020 valued at an annual level of $16 billion, would saddle individual market consumers, small businesses, state Medicaid programs, and Medicare Advantage enrollees with higher health care costs,

Can this be repealed?

Relief from the health insurance tax would result in real savings to the American people. We strongly urge Congress to provide an additional two-year suspension of the health insurance tax by passing H.R. 1398.

Calculates how the HIT affects your State and your business, here.

Take action now: tell Congress to repeal the HIT! Join small business owners across the country in stopping the HIT. Sign the petition here.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@medicalsolutionscorp.com.

EmblemHealth, formerly GHI and HIP, has recapitalized and reloaded dynamic plan offerings for 2019. They have had recent 3 years of single digit increases. Emblem has added significant new small group plans for 2019 thats fits the needs and budgets of small businesses. Each plan offers quality coverage with comprehensive benefits and network access.

New Expanded Prime Network: Access to a narrow and broad network

NYS – EmblemHealth has expanded small group Prime Network to include both the QualCare Network in New Jersey another ConnectiCare Network in Connecticut. This is in addition to the current HIP Prime Network in New York. Members can choose from over 90,000 private and group practice health professionals, facilities, and 144 hospitals in 28 New York State counties — all five boroughs of New York City (the Bronx, Brooklyn, Manhattan, Queens, and Staten Island), plus Nassau, Suffolk, Orange, Rockland, and Westchester counties, and upstate areas that stretch north of Albany.

CT – The ConnectiCare HMO Network has 17,000 primary care providers and specialists, and 33 hospitals in all eight counties in the State of Connecticut.

NJ – The QualCare HMO Network includes 26,000 primary care providers and specialists, and 76 hospitals in all 21 counties across the State of New Jersey.

New Select Care Network

It is a smaller subset of the larger Prime Network. It includes over 41,000 health care professionals, facilities, and hospitals throughout 28 counties in New York State. PRIME vs. SELECT NETWORK: Click Here

New Plan Features

3 free copays for PCP on selected plans.

Urgent Care no deductible

Labs no deductible

Adult & pediatric preventive dental no deductible

FREE Telemedicine through Teledoc. Members can get non-urgent medical care. It’s convenient, immediate, and available 24 hours a day, 365 days a year. Telemedicine doctors can even prescribe certain medicines.

FREE Acupuncture

Vision Included – free annual exam and lenses at 20% coinsurance.

Gym Reimbursements – up to $400 for member and $200 for spouse.

Emblem has been a NYS mainstay for 80 years. They insure 612,000 members. Notable clients are Union plans such as the NYC Teachers Union.

Sign up for upcoming webinars and newsletters. Please contact us TODAY for a customized analysis for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

The Google of health insurance?Oscar entered the NY market on Jan 1, 2014 and had around 16,000 members. In 2015, it expanded coverage to New Jersey and grew to about 40,000 members. In 2016, Oscar had 145,000 members in New York, New Jersey, California, and Texas. Oscar’s cutting edge technology and pioneering benefits have simplified the consumer health insurance experience propelled easier access and understanding of health plans. Examples of success have been ease of physician locator, online appointment setting and no cost telemedicine 24/7. Additionally, some plans have $0 Copay generics and annual 3 free office visits

The Numbers:

NY based with 900+ employees

260,000 members across 6 states

$890M raised from top investors (Fidelity, Goldman Sachs, Google, etc.)

$375M investment from Alphabet Inc. (Google parent company)

After doubling footprint for 2018,Oscar is on-track for 3x growth

Oscar Member Engagement:

27% of Oscar members utilize DocOnCall vs. industry average of 3%

35% of first time doctor appointments start with Oscar

3x customer satisfaction score vs. the industry average

48% of all Oscar members use the Oscar app, compared to 7% of other health insurance carriers

Doctor on Call has led to approximately $600 in savings per member

Concierge Team has led to an approx. $3,600 in savings in member OON claims

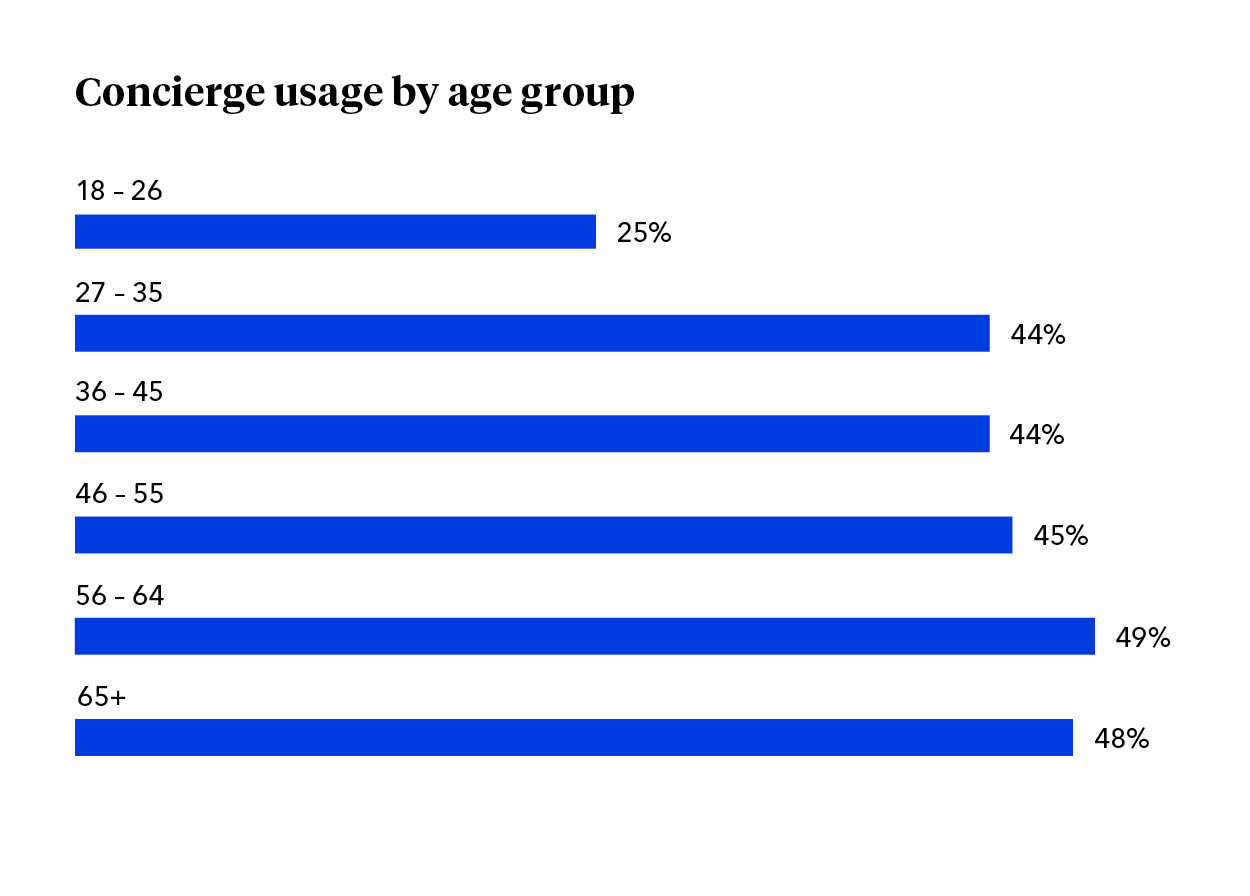

Pre-medicare population almost 2x Concierge Team utilization vs. the “younger” demographic

The Oscar Member Experience

Concierge Service: Every member is placed on a team of 5 care guides and 1 nurse that help members achieve better health outcomes and lower costs.

Doctor on Call: 24/7, free and unlimited telemedicine that works nationwide. This is a great way to care of basic primary care at the member’s convenience

New Oscar 2019

Oscar’s current network will be rebranded as Circle Network

15 plans across 4 metal tiers

NEWCircle Plus Network include:

Northwell (formerly North Shore LIJ)

Memorial Sloan-Kettering

Multiplan National Network for out of state

Westchester Expansion – Northern Westchester Hospital (Mt. Kisko), Phelps Hospital (Tarrytown) and the Westmed Medical Gorup added.

NEW: Only $0 deductible required Silver Plans!

Transitioning before 2019. Groups enrolling 11/1/19 can upgrade 1/1/19 to Circle Plus Network

NYS has approved 2019 Final Rates last Friday. Small group rates will increase 3.8% and 8.6% for individuals.

As per NY State Law, Health Insurers are required to send out early notices of rate request filings to groups and subscribers see original –NYS 2019 Rate Requests. Despite only 3 months of mature claims data experience for 2018 health insurers’ original requests were noticeably below average 7.5% for small group and 24% for individuals. Ultimately NYS reduced this request substantially by approximately 50%.

Experts are concerned over the long term effects. Example, the Individual mandate was removed last December by Presidential order. Without the Mandate anyone can drop insurance without penalty. A comparable take away for similar auto insurance industry would be something like this -Drivers ought not be mandated to buy auto insurance as its a profit scheme by Insurers. While a popular decision this will hardly bend the curve long term and reduce competition. Furthermore, the new order of Selling Across State lines makes NYS most unwelcoming.

OTHER STATES

Insurers have been filing to sell Obamacare plans that will go into effect in 2019, and in some states they appear to be pricing in for the fact that the mandate is going away next year. Other states are seeing mild increases, but that is in part because they saw significant hikes for the previous year.

Insurers have concluded that fewer people will enroll without the mandate than otherwise, so in some places they are pricing their plans higher based on the assumption that sicker people will be left behind, which will increase medical costs for those left. It is well worth pointing out that in recent years the loss federal risk reinsurance corridor funds account for 5.5 percent of the rate increase.

How are neighboring States doing?

In NJ, not that bad. Last year the average increase were 5.5% for small groups and some popular plans such as Horizon Blue Cross Blue Shield’s OMINA increasing only 4.8% increase. This year the increase is only 5.2. Other insurers offering EPO and HMO plans in the individual market for 2019 include Oscar Health and Oxford Health Plans.

With individual mandate repeal fewer people will buy health insurance raising the prices for those who do. NJ Banking and Insurance Department officials said premium prices would have increased, on average, by 12.6 percent.

For CT market, on the other hand, things are much worse at least for the individual marketplace with average 25% rate increases last year. The 2019 proposed rate increases for both the individual and small group market are, on average lower, than last year: The proposed average small group rate increase request is a 10.22 percent and ranges from -5.0 percent to 21.1 percent. This compares to the average increase request of 18.06 percent requested last year.The proposed average individual rate increase request is 12.3 percent and ranges from -10.9 percent to 31.0 percent. This compares to the average increase request of 25.51 percent requested last year.

Final plan rates in New Jersey & CT will be finalized and released in the fall, state officials said. ACA open enrollment begins Nov. 1

Trend: Trend is a factor that accounts for rising health care costs, including the cost of prescription drugs, and the increased demand for medical services.

Uncertainty in Washington:

Removal of penalty for individual mandate: The elimination of the penalty means that individuals who are typically younger and healthier would have no inducement to participate in the insurance pool, which could further destabilize the market. Lack of participation shrinks the pool and increases the cost of insurance to the remaining members.

Short-duration health plans and Association Health Plans: Still pending are final federal regulations on non-ACA compliant short-duration plans, which may have implications for the ACA risk pool. Also, Connecticut along with other state insurance regulators, are awaiting clarification from the federal government on new federal regulations allowing association health plans, which could further shrink the ACA risk pool.

A bipartisan group of congressional representatives has discussed an agreement to extend and guarantee the payments, but it’s unclear whether they could do so by the new filing deadline of Sept. 5. A lawsuit filed by Congress against the Obama administration to challenge the payments is still pending. In addition, Trump has repeatedly threatened to withhold payments to insurers that reduce cost-sharing – deductibles, copays and coinsurance – paid by low-income customers. More than half of New Jersey’s marketplace customers receive that assistance, and without it, most would be unable to afford coverage.

Finally, a tax on health insurance premiums has been reinstated in 2018 after a one-year “tax holiday” approved by Congress for 2017. That contributed 2.3 percent to the rate hikes that insurers requested for 2019 and for 2019

SMALL GROUP MARKET VS. INDIVIDUAL MARKET

Importantly, small group market is still more advantageous than individual markets unless one gets a sizable low-income tax credit. Overall, about 350,000 individual plan consumers will be affected by the price hike, while more than a million users will be hit by higher small group fees. Last year, Blue Cross Blue Shield released a study showing Obamacare user costs were 22 percent higher than people with employer-sponsored health plans, while UnitedHealthplans to exit most Exchanges see – Breaking: Oxford Exits Metro Indiv & Oxford Liberty HMO 2017.

The correct approach for a small business in keeping with simplicity is a Private Exchange and with our large buying group PEO partnerships. This is a true defined contribution empowering employees with a choice of leading insurers offering paperless technologies integrating HRIS/Benefits/Payroll. Both employee and employers still gain tax advantage benefits under the business. Also, the benefits, rates and network size are superior under a group plan as the risk are lower for small group plans than individual markets.

Learn how a Private Exchange and our PEO Partnership can help your group please contact us at info@medicalsolutionscorp.com or (855)667-4621.

Last Friday, June 1, 2018, the NYS 2019 Rate Requests filings were released. Great news for SMB! The total weighted average increases were a modest 7.5% small groups but 24% for the individual market. This early filing request deadline request requirement is not an Obamacare requirement. As per NY State Law carriers are required to send out notices of rate increase filings to groups and subscribers.

These are simply requests and the state’s Department of Financial Services has authority to modify the final rates. But they are the first indication of what New Yorkers can expect when shopping for health insurance on the individual marketplace at the end of this year. The news comes as insurance companies across the country brace consumers for another year of large rate hikes, owing in part to the composition of the individual market, and in part to the uncertainty over the future of the law under the Trump administration.

Background:

By contrast last year’s NYS 2018 Rate Request early filing request were higher at 11.5% small group but much lower 16.6% for individuals. The NYS final August 2018 rate approval are expected to be lower. For example, the final filing rates were aproved NYS 2018 Final Rates at 9.3% small group and 13.9% for individuals. Incidentally, the NYS 2017 Rates final rates were 8.3% small group and 12.3% for individuals. Using these past figures one projects a 2019 Final Rates of 6.5% small groups and 19% individuals.

With only 3 months of mature claims in 2018 to work of off Insurance Actuaries have little experience to predict accurate projections. Simply put the less credible information presented to actuarial the higher the uncertainty and higher than the expected rate increase. The national rate trend, however, has been much higher than in past years due to higher health care costs and the loss of Federal reinsurance fund known as risk reinsurance corridor.

Summary of 2019 Requested Rate Actions

Individuals:

Individual rates are expected to be higher than the small group market. The national rate trend, however, has been much higher than in past years due to higher health care costs Like other states throughout the nation, the 2019 rate of increase for individuals in New York is higher than in past years partly due to the termination of the federal reinsurance program. The loss of the program’s aka federal risk reinsurance corridor funds accounts for 5.5 percent of the rate increase.

The single biggest justification offered by insurers for the requested increases is the recent repeal of the individual mandate penalty –Tax Reform Bill Includes Repeal of Individual Mandate Beginning in 2019. The individual mandate, a key component of the Affordable Care Act, helped mitigate against dramatic price increases by ensuring healthier insurance pools. Insurers have attributed approximately half of their requested rate increases to the risks they see resulting from its repeal. Without the federal action, the average requested rate increase would be 12.1%. As DFS reviews all of the submissions, we will continue to ensure that any rate increases are fully and actuarially justified by appropriate medical cost increases and are not inadequate, excessive or unfairly discriminatory, in accordance with New York law.

Small Groups:

Most encouraging to see the average rate requests for the small group market reflect the increased stability of that market in New York State. The combination of 2-50 and 51-100 market underscores the stability for msall bsuinesses under 50 employees. Prior to the NYS regulatory combination, the 2-50 market was running an average 12-13% trend.

The Obamacare health insurance tax, aka The HIT, is responsible for approximately 2.5%. Whiel the HIT moratorium was approved it had indeed come back last year. The total projection is $14 Billion. Notably, Empire Blue Cross has filed a modest 6% increase as their portfoliio is running stable. Additionaly, Oscar’s inbdustry low 3% filing is practially at break-even considering the HIT.

THE THREE R – RISK CORRIDOR, RISK ADJUSTMENT & REINSURANCE designed to mitigate the adverse selection and risk selection. The problem, according to many insurance companies, is that the formula is flawed, and CareConnect executives have consistently complained that they are at an unfair disadvantage. The Cuomo administration has taken steps to ameliorate some of those problems, giving the DFS the authority to essentially overrule the federal numbers. In its first-quarter financial report, executives made clear that the risk adjustment penalty was a threat to its business.

Company Name

2019 Requested Rate Change

Aetna Life

16.2%

CDPHP

6.7%

CDPHP UBI

6.1%

Crystal Run Health Insurance Company

11.5%

Crystal Run Health Plan, LLC

12.5%

Emblem

12.0%

Empire Healthchoice Assurance

6.0%

EmpireHealthchoice HMO

5.2%

Excellus*

3.8%

Healthfirst Health Plan, Inc.

21.0%

Healthfirst Insurance Company, Inc.

7.0%

Healthnow New York

-0.1%

IHBC*

3.8%

MetroPlus*

4.7%

MVP Health Plan

7.0%

MVP Health Service Corp*

10.3%

Oscar

3.0%

Oxford Health Insurance Inc*

8.3%

UnitedHealthcare Ins Company of New York

7.2%

Weighted average:

7.5%

Conclusion

Defined Contribution Choice: Instead, the correct approach for a small business in keeping with simplicity is a defined contribution model using a PrivateExchange. This is a true defined contribution empowering employees with the choice of leading insurers offering paperless technologies integrating HRIS/Benefits/Payroll. Both employee and employers still gain tax advantage benefits under the business. Also, the benefits, rates and network size are superior under a group plan as THE RISK OUTLINED ABOVE ARE HIGHER FOR INDIVIDUAL MARKETS THAN SMALL GROUP PLANS.

To be clear: These trends affect a small subset of the insurance market—non-group plans that cover less than 2 percent of the population. Many qualify for tax credits that lower their net costs and reduce or eliminate the impact of year-to-year rate increases.However, non-group customers with incomes above 400% of the poverty level ($48,560 for a single adult) get no subsidy—and feel the full brunt of any hikes.

Resource

You may view the NYS 2019 Rate Requests DFS press release, which includes a recap of the increases requested and approved by clicking here.

For a custom analysis detailing YOUR upcoming 2018-2019 renewal please contact our team at Millennium Medical Solutions Corp (855)667-4621. We work in coordination with Navigators to assist with Medicaid, CHIP Child Health Plus, Family Health Plus and Medicare Dual Eligibles. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed onour site.

Survey Shows 94% of PEOs Expect an Increase in Employees

Businessman pressing a People concept button.

Professional Employer Organizations (PEO) growth doesn’t appear to be slowing down. Earlier this year, NAPEO released the results from there 2017 Q3 Industry Pulse Survey. The findings showed that PEOs are continuing to grow, and at an impressive pace. In the report, 72% of PEOs reported revenue growth in Q3 of 2017, compared to Q3 of 2016.

With all that is happening with employment laws, healthcare and health insurance, and other areas of HR that impact small and medium-sized businesses (SMBs), it is easy to see why PEOs and other HR outsourcing options are seeing, in many cases, rapid industry growth.

Now, NAPEOs latest Quarterly Pulse Survey, which compared the 4th quarter of 2017 to the 4th quarter of 2016, shows that PEO growth is still occurring, and will almost certainly continue in 2018 and beyond.

DATA FROM THE 2017 Q4 NAPEO PULSE SURVEY

The NAPEO Quarterly Pulse Survey – Q4 2017 was conducted in early 2018, and was taken by 32 PEO executives.

The first result from the survey looked at PEO revenue. 71.9% of PEO executives said their organization’s revenue increased in Q4 of 2017, compared to Q4 of 2016.

Broken down further, 50% said that revenue increased somewhat, and 21.9% said revenue increased significantly.

Next, the survey showed that PEOs experienced an increase in the average annual wage per worksite employee (WSE), with 65.5% of executives responding.

NAPEO’s findings also revealed that 66% of PEOs saw an increase in gross profit. Of this 66%, 43.3% said gross profit increased somewhat, while 23.3% said it increased significantly.

OPERATING INCOME, NUMBER OF CLIENTS, AND WSE PROJECTION DATA

The next group of results from the survey uncovered data around operating income, the number of clients, and worksite employee projection information.

First, the report showed that 65.7% of PEO executives reported an increase in operating income in the 4th quarter of 2017, compared to the 4th quarter of 2016. The 65.7% can be broken down further, with 43.8% saying that operating income increased somewhat, and 21.9% increasing significantly.

Next, 59.4% of PEOs said that the number of clients increased, while 31.3% said that the number of clients stayed about the same. Of the 59.4%, 50% said that clients increased somewhat, and 9.4% said clients increased significantly.

Lastly, the survey asked PEO executives about worksite employee (WSE) projections over the next 12 months.

Perhaps the most promising and impressive statistic found in the quarterly survey, almost 94% expect WSEs to increase. Here is the full breakdown:

71% expect EE to increase somewhat

22.6% expect EE to increase significantly

3.2% expect EE to stay about the same

3.2% expect EE to decrease somewhat

With PEOs seeing an increase in revenue throughout 2017, and executives overwhelmingly expecting EE to increase over the next 12 months, revenue outlooks for the rest of 2018 and into 2019 look extremely promising throughout the PEO industry.

PROFESSIONAL EMPLOYER ORGANIZATIONS CONTINUE TO THRIVE

Much like the last few Quarterly Pulse Surveys from NAPEO, the 2017 Q4 survey shows that despite all of the uncertainty and complexity with various areas of HR, PEOs continue to grow.

Regarding the survey, Pat Cleary, President & CEO of NAPEO, said, “This is just the latest example that more and more business owners are realizing the true value of using a PEO. Surveys and studies consistently show that using a PEO is good for a business and its employees. PEOs provide a real benefit to businesses by providing HR services and solutions that they would otherwise be unable to afford.”

Some additional findings from the survey include:

Average annual wage per WSE increased somewhat

Average number of WSEs per client company stayed about the same

Number of internal employees (including salespeople) stayed about the same

Number of Worker’s Compensation claims reported to carrier stayed about the same

The survey also revealed that the average PEO has 19 worksite employees per client.

Learn how a PEO can help grow your business. Check out PEO Case Studies here and learn how they can apply to you.

Click below for a free PEO assessment. OurPEO Quoting Tool ensures that we have first-hand insight as to what the small business owner needs to be successful.